Electric vehicles (EVs) are increasingly recognized as a crucial component in the global effort to achieve the Sustainable Development Goals (SDGs) set by the United Nations. The SDGs are a collection of 17 interlinked global goals designed to be a "blueprint to achieve a better and more sustainable future for all" by 2030. EVs specifically intersect with several of these goals, offering a pathway to a more sustainable and environmentally friendly future.

First and foremost, EVs contribute significantly to SDG 7, which is focused on ensuring access to affordable, reliable, sustainable, and modern energy for all. By transitioning from fossil fuel-powered vehicles to EVs, we can significantly reduce reliance on non-renewable energy sources. This shift is crucial because the transport sector is a major consumer of energy, and a significant portion of global energy consumption comes from non-renewable sources like oil. EVs, which can be powered by renewable energy sources such as solar or wind power, represent a more sustainable alternative.

Another critical SDG impacted by the rise of EVs is SDG 13, which calls for urgent action to combat climate change and its impacts. Traditional vehicles powered by internal combustion engines are a major source of greenhouse gas emissions, contributing to global warming and climate change. EVs, on the other hand, emit significantly fewer greenhouse gases, especially when charged with electricity from renewable sources. Therefore, the widespread adoption of EVs can be a vital part of efforts to reduce emissions and mitigate climate change.

The relationship between EVs and SDG 9, which focuses on building resilient infrastructure, promoting inclusive and sustainable industrialization, and fostering innovation, is also noteworthy. The development and widespread adoption of EVs require significant innovation in areas such as battery technology, electric motor systems, and charging infrastructure. This innovation not only drives progress in the automotive industry but also stimulates economic growth and job creation in new and emerging sectors related to EV technology.

EVs also play a role in achieving SDG 11, which aims to make cities and human settlements inclusive, safe, resilient, and sustainable. One of the key challenges in urban areas is managing air quality. Emissions from traditional vehicles contribute to air pollution, which has significant health impacts. By replacing these vehicles with EVs, cities can significantly improve air quality, leading to better health outcomes for their residents.

Furthermore, EVs tie into SDG 12, which is about ensuring sustainable consumption and production patterns. The automotive sector has long been associated with unsustainable consumption due to the reliance on non-renewable resources and the environmental impact of vehicle emissions. EVs offer a more sustainable model of consumption and production, especially when paired with a circular economy approach where EV batteries are recycled and repurposed.

Lastly, the global transition to EVs also indirectly affects other SDGs, such as SDG 8 (Decent Work and Economic Growth) by creating new job opportunities in renewable energy sectors, and SDG 3 (Good Health and Well-being) by reducing pollution-related health issues. However, it's important to note that the transition to EVs also presents challenges, such as the need for raw materials for batteries and the development of adequate charging infrastructure, which must be addressed responsibly and sustainably.

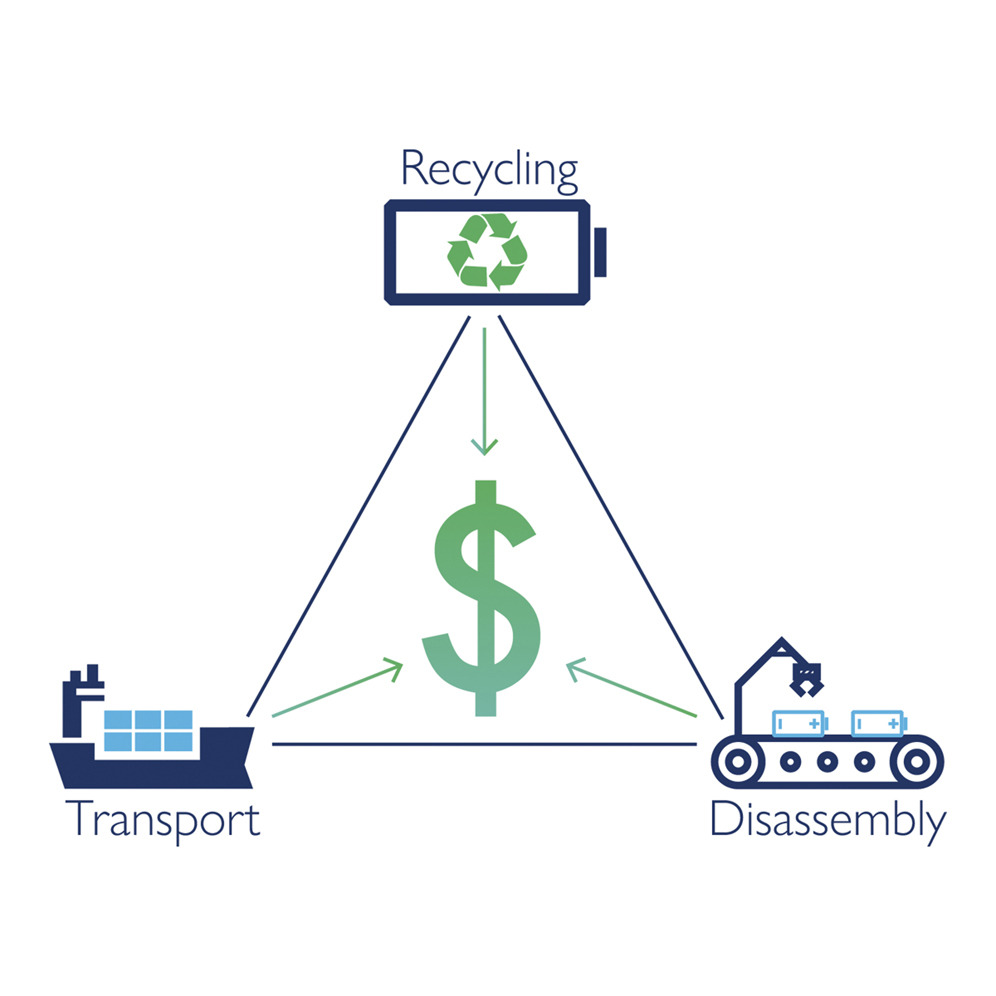

Economically viable electric vehicle lithium-ion battery recycling is increasingly needed; however routes to profitability are still unclear. We present a comprehensive, holistic techno-economic model as a framework to directly compare recycling locations and processes, providing a key tool for recycling cost optimization in an international battery recycling economy. We show that recycling can be economically viable, with cost/profit ranging from (−21.43 - +21.91) $·kWh−1 but strongly depends on transport distances, wages, pack design and recycling method.

Despite the improvement in technologies for the production of alternative fuels (AFs), and the needs for using more AFs for motor vehicles for the reductions in air pollution and greenhouse gases, the number of alternative fuel vehicles (AFVs) in the global transportation sector has not been increasing significantly (there are even small drops for adapting some AFs through the projections) in recent years and even in the near future with projections to 2050. And gasoline and diesel fuels will remain as the main energy sources for motor vehicles.

Electric vehicles (EVs) are widely regarded as the key to finally making private mobility clean, yet virtually no research is being conducted on their potential contribution to the expansion of impervious surfaces. This study aims to start a discussion on the topic by exploring three relevant issues: the impact of EVs’ operating costs on urban size, the space requirements of charging facilities, the land demand of energy production through renewables.

Wolf-Peter Schill is Deputy Head of the Energy, Transportation, Environment Department at the German Institute for Economic Research (DIW Berlin), where he leads the research area Transformation of the Energy Economy. He engages in open-source power sector modeling, which he applies to economic analyses of renewable energy integration, energy storage, and sector coupling. He holds a diploma in environmental engineering and a doctoral degree in economics from Technische Universität Berlin.

Electric Vehicles for Smart Cities, Trends, Challenges, and Opportunities, 2021, Pages 181-247

The future role of stationary electricity storage is perceived as highly uncertain. One reason is that most studies into the future cost of storage technologies focus on investment cost. An appropriate cost assessment must be based on the application-specific lifetime cost of storing electricity. We determine the levelized cost of storage (LCOS) for 9 technologies in 12 power system applications from 2015 to 2050 based on projected investment cost reductions and current performance parameters.

The development of new high-efficiency magnets and/or electric traction motors using a limited amount of critical rare earths or none at all is crucial for the large-scale deployment of electric vehicles (EVs) and related applications, such as hybrid electric vehicles (HEVs) and e-bikes. For these applications, we estimated the short-term demand for high-performing NdFeB magnets and their constituent rare earths: neodymium, praseodymium and dysprosium. In 2020, EV, HEV and e-bike applications combined could require double the amount used in 2015.